|

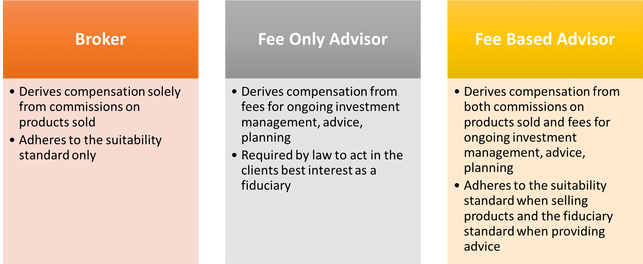

Most professions have a measuring stick to quantify a reputation or skill set. Medical degrees, law degrees and teaching certificates represent recognizable benchmarks for their professions. Our proud service men and women use a chain of command that instantly indicates their level of responsibility. So why is it so difficult to determine whether or not a financial advisor is worth their salt? The term “Financial Advisor” may very well be one of the most misrepresented professional titles. Reason being: Almost anyone can call themselves one. Don’t get me wrong, the financial services industry puts numerous exams and stipulations in place to license and track advisors, but just like any standardized test a passing score isn’t necessarily a great barometer for quality. According to WalletHub there are over 250 thousand advisors across the country. Thankfully, there are ways to help you to determine the background, experience and type of advisors out there. Professional designations such as the CFP® (Certified Financial Planner), CFA (Chartered Financial Analyst®) and the already recognizable CPA, (Certified Public Accountant) give consumers a basic understanding of the training someone has endured. In any vetting process, educational background combined with a professional designation is one of the first things to look for. It’s not to say the absence of one is bad. I know many advisors who do a good job for their clients and don’t have letters after their name, which brings me to my next point. Experience. Type can often be more valuable than tenure. While it’s comforting to see lots of years in the industry, that experience may not add up to a whole lot of knowledge. Here’s a shocker: Some financial services organizations allocate more resources to sales training than education. A good way to decipher experience from fluff is to interview. Just like any job interview, pointed open-ended questions help to uncover details. What types of clients have you worked with? What is your investment philosophy and why? Situational questions such as, “tell me about the message you were sending to your clients back in 2008 and 2009 during the financial downturn,” provide a window into what the experience and expectations could look like. Background. Finance is one of the most regulated industries on the planet largely because it involves money management. A background check is a great way to examine an advisor’s experience, licensing and whether or not any complaints have been filed against them. FINRA (Financial Industry Regulatory Authority) provides a great reference tool. Hint: It will also help you to recognize the different types in the next topic. The Landscape of Financial Professionals  There’s a difference between suitability and fiduciary. Similar to the Hippocratic oath to do no harm that a licensed physician takes, a fiduciary is bound by law to act in your best interest. Believe it or not, this isn’t a requirement for most financial advisors. Reason being; if they sell commissionable products, the only obligation is to make sure that the product is suitable for the investor. The phraseology here is interesting. If you were to ask an investor which they would prefer: something that was in their best interest or something that was merely suitable for them, you would likely receive resounding support for the former. Consider the idea of a doctor being solely compensated based upon the treatments or medicines they recommended. The conflict of interest would instantly be apparent. Entering into an engagement with an advisor, whose compensation was based upon the commission from a product sale, isn’t a heck of a lot different from this scenario. The incentives often work in the opposite direction of what's in your best interest, even if they're trying to do the right thing. As fiduciaries, Fee-Only Registered Investment Advisors receive zero commissions because the only product they have to sell is their expertise, something that is quantifiable and transparent, as opposed to sales commissions which are often wrapped into the complexities of a financial products expenses. It’s important to point out the dilemma that Fee-Based Advisors face. Namely, when is it appropriate to sell products to a client based on a standard or suitability, and when is it appropriate to provide advice as a fiduciary acting in their best interest? Many see this as a contradiction. Why wouldn’t someone want to act in my best interest all the time? It’s the critical question that should be asked of every financial professional. Hopefully this sheds some light on a confusing topic. A word of advice would be to know what type of advisor you are speaking with before you even interact with them. Due diligence up front is key because in a business populated by a litany of salespeople, judgment can sometimes get cloudy after a face to face meeting. Financial professionals are always being mischaracterized partly due to an industry that intentionally blurs the lines. Most true Fee-Only Financial Advisors loathe being inadvertently called Brokers, and Brokers often do little to clarify that they aren’t actually acting in a fiduciary capacity. I’m not sure if we’ll ever get away from blanket terminology, but I am sure that individual investors are better served when they’re empowered with the knowledge to make informed choices. *Photo Courtesy of CFP®Board

Comments are closed.

|

|

Phone: 860-837-0303

|

Message: [email protected]

|

|

WINDSOR

360 Bloomfield Ave 3rd Floor Windsor, CT 06095 |

WEST HARTFORD

15 N Main St #100 West Hartford, CT 06107 |

SHELTON

One Reservoir Corporate Centre 4 Research Dr - Suite 402 Shelton, CT 06484 |

ROCKY HILL

175 Capital Boulevard 4th Floor Rocky Hill, CT 06067 |

Home I Who We Are I How We Invest I Portfolios I Financial Planning I Financial Tools I Wealth Management I Retirement Plan Services I Blog I Contact I FAQ I Log In I Privacy Policy I Regulatory & Disclosures

|

|

|

|

|

|

|

© 2024 WealthShape. All rights reserved.